Over the past few years, something has quietly changed in the IUL space.

More and more policies are no longer linked to traditional indices like the S&P 500.

Instead, they’re linked to:

- Multi-asset indices

- Volatility-controlled indices

- Proprietary or “custom” indices

And if you’ve seen any recent illustrations, you’ll notice something:

👉 The projected returns often look… very attractive.

At First Glance, It Looks Like an Upgrade

Compared to the S&P 500, these indices often show:

- Smoother performance

- Higher backtested returns

- Less volatility

Which naturally leads to the question:

“If this looks better, why would anyone still use the S&P 500?”

This Is Where It’s Important to Pause

Because what you’re looking at is not just performance.

👉 You’re looking at how that performance was constructed.

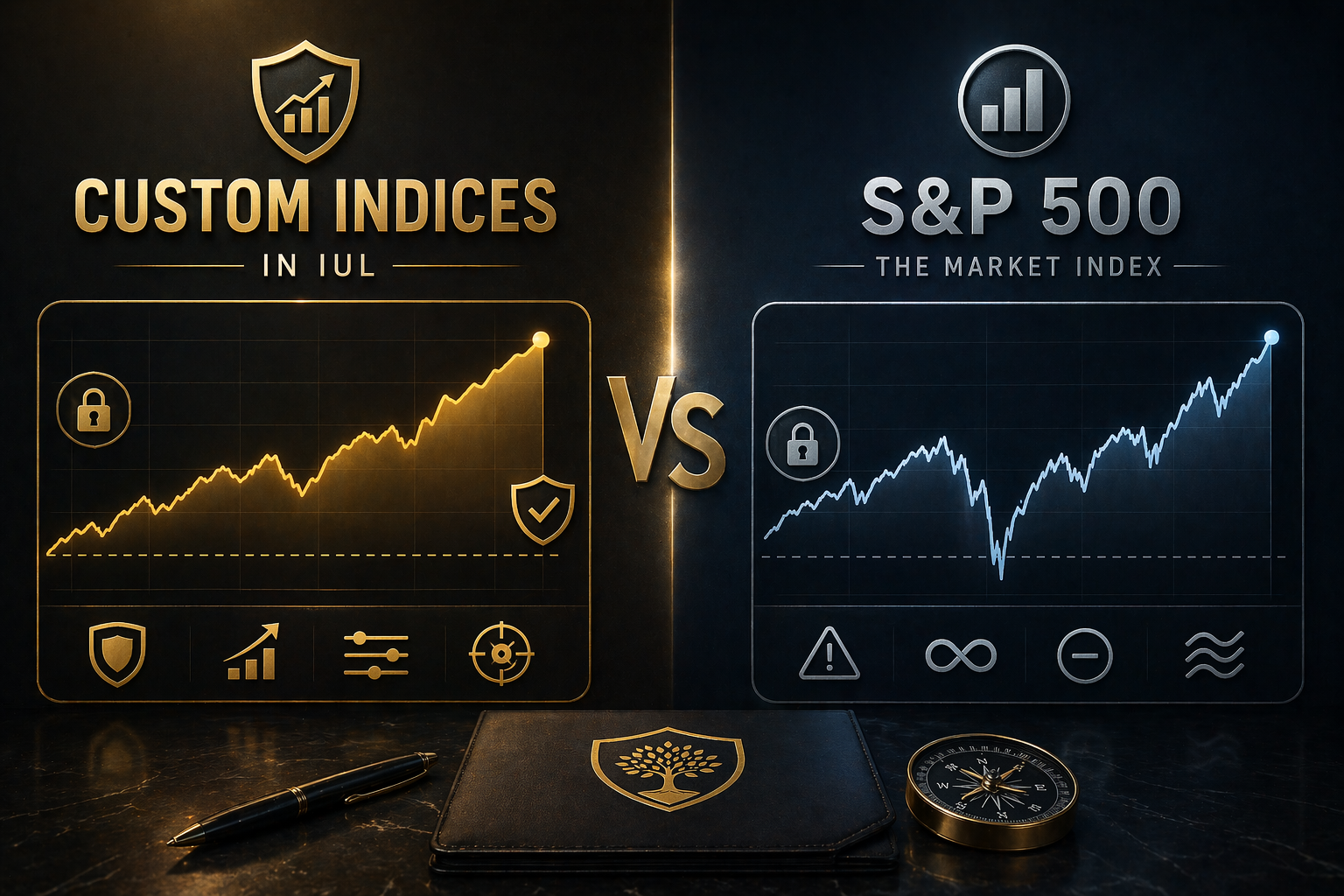

The Key Difference Most People Miss

Let’s separate this clearly.

S&P 500

- Real, live market index

- Decades of actual historical data

- Publicly trackable

You can:

- Check it anytime

- Verify past performance

- Understand what drives it

👉 In simple terms:

What you see is what has actually happened.

Custom Indices

This is where things become less straightforward.

Most custom indices:

- Are relatively new

- Have limited real-world track records

- Rely heavily on backtested data

👉 And this is the key point:

Backtested data is not the same as real performance.

What Backtesting Actually Means

Backtesting works like this:

- A strategy is designed today

- Historical data is applied to simulate past performance

- The results are presented as if the strategy existed before

👉 On paper, this can look very strong.

Because the strategy is often:

- Optimised using past data

- Structured to perform well under specific conditions

But There’s a Limitation

Backtesting answers one question:

👉 “How would this have performed in the past?”

But it doesn’t answer:

👉 “How will this perform in the future?”

And more importantly:

👉 It doesn’t account for:

- Changing market conditions

- Real-time execution constraints

- Behaviour during unexpected events

Why This Matters in Practice

When clients look at illustrations, it’s easy to assume:

“If it performed this way historically, it should perform similarly going forward.”

But when that performance is based on:

- Hypothetical modelling

- Strategy optimisation

- Limited real-world data

👉 Expectations can become disconnected from reality.

The Role of Volatility Control (Another Layer)

Many custom indices include volatility control mechanisms.

This means:

- When markets become volatile → exposure is reduced

- When markets stabilise → exposure may increase

👉 The intention is to create smoother outcomes.

But over time, this can also:

👉 Limit participation during strong market recoveries.

So What Are You Really Buying?

This is the question that matters most.

With S&P 500-based IUL:

- You are tied to a real market benchmark

- You can verify performance independently

- You understand what drives outcomes

With Custom Index-based IUL:

- You are relying on a constructed strategy

- Performance is influenced by design decisions

- Transparency is more limited

Why S&P 500-Based Policies Often Look Less Attractive on Paper

This comes up often.

When comparing illustrations:

- S&P 500-based policies may show lower projected returns

- Assumptions tend to be more conservative

👉 Which makes them appear:

Less “optimised”

But there’s a reason for that.

👉 The projections are grounded in actual, observable market behaviour

—not simulated optimisation.

A Pattern I’ve Noticed Over Time

Clients who prioritise:

- Transparency

- Verifiability

- Long-term clarity

…tend to lean towards simpler, more established benchmarks like the S&P 500.

While clients drawn to:

- Higher projections

- Smoother illustrations

…may initially gravitate towards custom indices.

This Doesn’t Mean Custom Indices Have No Role

They were created for a reason:

- To manage volatility

- To provide smoother crediting patterns

But it does mean:

👉 You are making a trade-off.

A More Grounded Way to Decide

Instead of focusing purely on projected returns, it may be more useful to ask:

- Is this based on real or simulated performance?

- Can I independently verify this index?

- How long has this index existed in real conditions?

- What assumptions are embedded in the design?

Because Ultimately…

An index is not just a performance number.

👉 It’s a framework that determines how returns are generated.

Final Thought

Higher projected returns can be appealing.

But over the long term:

👉 Transparency tends to age better than optimisation.

And understanding whether your returns come from real markets

or constructed models

makes all the difference.

If you’re reviewing IUL options and comparing different index strategies, it may be worth understanding not just the projected returns — but how those returns are actually derived.

👉 If you’d like a clearer breakdown of how different index options may impact your policy, feel free to reach out via WhatsApp